In the early stages of investing, progress feels painfully slow.

You’re putting money aside each month, investing consistently into the market and doing all the right things – but the results don’t always feel meaningful. £5,000 becomes £10,000. £10,000 becomes £25,000. Yes, it’s progress, but it doesn’t quite feel life-changing. Building an investment portfolio that will allow you to comfortably retire still feels like a distant dream.

Whatever you do, don’t stop. You need to get your hands on £200,000 and then you can take your foot off the gas (and perhaps stop driving altogether).

Why £200k is an important investing milestone

Charlie Munger once famously said: “The first $100,000 is a bitch, but you gotta do it. I don’t care what you have to do. If it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.“

This was in the late 1990s, and adjusted for inflation, this number would be worth ~$200,000 in March 2026 dollars. For simplicity, we’ll call it £200,000.

So, Charlie Munger, one of the greatest investors of all time and Warren Buffett’s business partner, said it was a priority to get your hands on £200,000. Why?

Well, a portfolio at around this value will start to generate significant annual returns, assuming it’s invested in diversified index funds. At 9% annual returns, a £200k portfolio will generate £18,000 per year in growth (on average). For many people, this is the same range (or more) than what they’re able to invest annually. In other words, your portfolio is now contributing more than you are. With contributions included, your portfolio grows more quickly and progress accelerates.

Up to £200k, progress has largely been driven by your savings rate. You’ll start to experience compounding beyond £100k, but at £200k the real growth starts. Suddenly, you’ll find your investments pushing you to a higher and higher net worth quicker than you could have ever imagined. Motivation increases, and the early retirement you’ve been dreaming of now seems a lot more tangible.

What compounding really looks like

The power of compounding is often talked about, but rarely felt in the early years. That’s because compounding needs two things: time and a meaningful base. £200k is that base.

It’s the point where compounding stops being theoretical and starts being visible.

The graphic below shows what happens when you simply leave £200,000 invested at 9% annual returns, with varying levels of additional contributions:

Even with no additional contributions, the portfolio grows to nearly £18 million over 50 years. This is the first key insight: you don’t need to keep pushing forever – just build a base and give it time.

The Crossover Point

£200k is the point where your investment returns begin to rival or exceed your annual contributions. This is sometimes called the crossover point (another definition is when your investment returns exceed your salary).

Before this point, contributions drive growth, but after this point, compounding drives growth. This is what makes £200k so powerful: it’s the point where the system you’ve built starts running on autopilot.

Once you reach this point, you may then start to wonder if you need to invest as aggressively. Your instinct may be to keep pushing – to maximise every contribution until you reach your retirement goal.

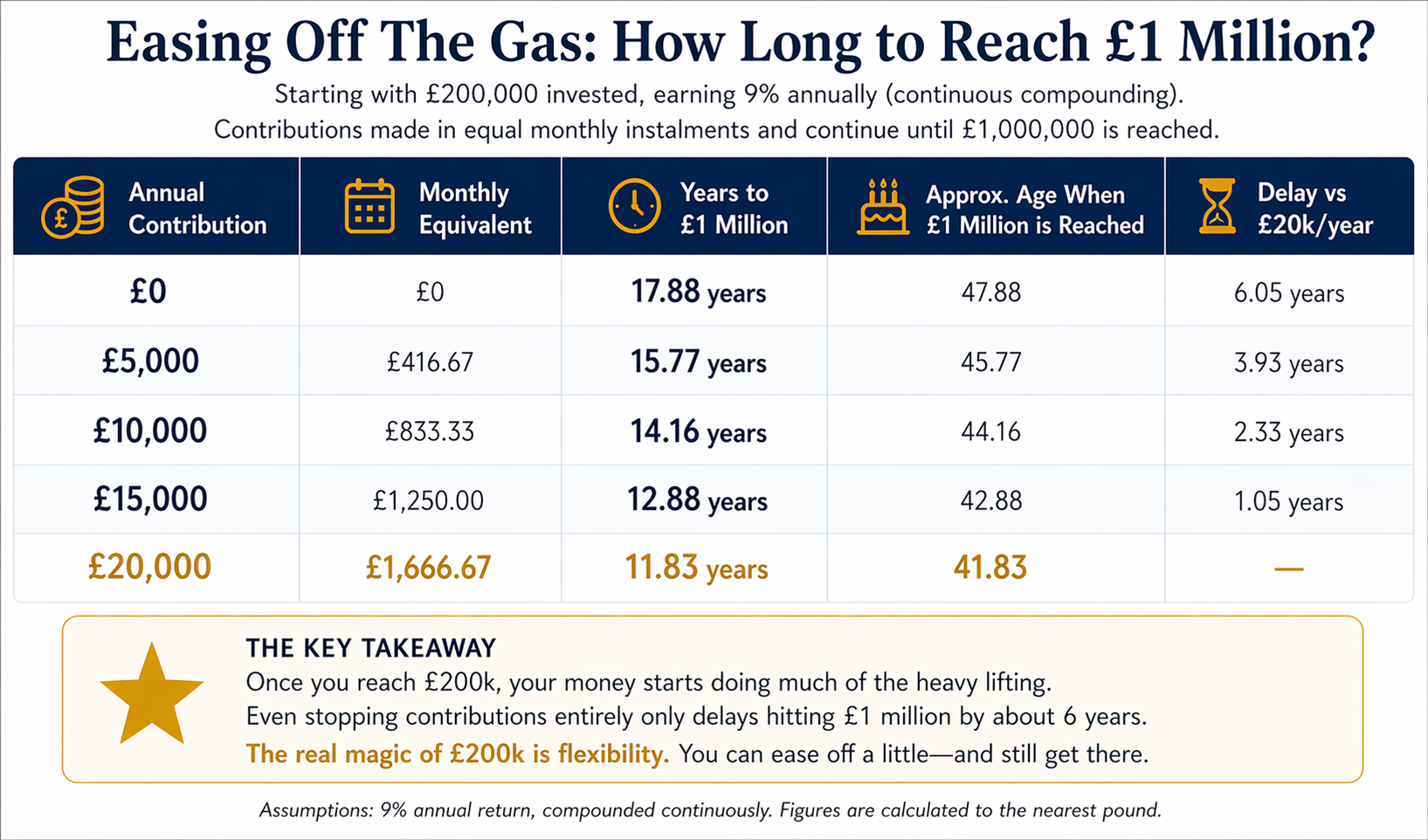

But the numbers tell a different story. Here’s what happens when you vary your annual contributions starting from £200k:

A few things stand out immediately:

- Even with no further contributions, you still reach £1 million in under 18 years.

- Reducing contributions from £20k to £10k only delays the outcome by around 2 years.

- Stopping contributions entirely delays it by around 6 years.

We can make a fair assumption that in order to reach £200k, you’d be saving and investing aggressively, perhaps maxing out your £20k ISA limit each year. What this means is that you can essentially cut your savings rate in half and it will hardly change the time it takes to reach a cool £1 million. In other words, you can cruise to the finish line after £200k.

Reducing contributions or stopping them entirely has far less of an impact than most people expect.

Why the impact of contributions shrinks

At smaller portfolio sizes, contributions are everything. If you’re investing £10,000 per year into a £20,000 portfolio, your contributions dominate the outcome. But at £200k and beyond, the dynamic changes.

At 9%:

- £200k generates £18k/year.

- £500k generates £45k/year.

- £1m generates £90k/year.

At this point, your contributions – even at £20k or more – become relatively small in comparison. That’s why easing off the gas has a smaller impact than expected – the engine is already on cruise control.

What this means in real life

This is where investing becomes less about optimisation, and more about designing your life. Reaching £200k doesn’t just give you financial momentum, it gives you options.

You can:

- Reduce your savings rate.

- Change careers.

- Work fewer hours.

- Take extended time off.

- Spend more on experiences that matter to you.

And still make long-term progress. That’s the real value of this milestone.

The hidden benefit: psychological momentum

There’s also something less tangible, but equally important. Momentum.

Before £200k, investing feels like effort without reward. After £200k, progress becomes more visible.

The numbers move faster, growth becomes more noticeable and the journey feels real. And because you can finally see the system working, your behaviour changes.

It becomes easier to:

- Stay invested.

- Ignore short-term noise.

- Think long-term.

Because successful investing is more about managing your emotions than being able to pick the right fund or stock, this more noticeable growth makes it easier to stay invested.

Conclusion

£200k isn’t magic in a mathematical sense, but it feels magical because it marks the point where investing begins to work with you rather than against you. In the early years, progress is driven almost entirely by your own effort – your savings rate, your discipline, and your ability to stay consistent even when the results feel slow. But once you reach this level, something shifts: compounding becomes visible and growth becomes meaningful. And the portfolio you’ve built starts to generate returns that are large enough to rival your own contributions.

This is what creates the sense of momentum. Investing no longer feels like a grind where every pound must be earned and added manually. Instead, it becomes a system that begins to run independently, quietly building in the background while you focus on other aspects of your life. That’s why £200k matters so much – not because it represents an end point, but because it represents a starting point.

Thanks for reading! Here are some other articles you may enjoy:

- The 4% Rule – how to know when to retire

- How to make the most of your ISA

- How to Make the Most of Your Workplace Pension

- Retire Early by Not Being a Moron with Your Money

- The Best Paycheque Routine to Save, Invest and Build Wealth

- The Major Money Milestones as you Build Wealth

You can follow me on X, and find me on Pinterest, Instagram and Facebook.

Leave a Reply