In the early years of your investment journey, progress feels slow. Every pound saved is hard-earned, and the gap between where you are and where you want to be feels enormous. But as the portfolio grows, there’s a moment in the journey when things begin to feel different. Compounding begins to take hold, giving your portfolio growth more and more momentum, and eventually exceeding the money you earn. This is called the Crossover Point.

By this stage, the question changes from “How do I build wealth?” to “Can I ease off the gas a bit?” At large portfolio sizes, the answer is most definitely yes. Let me explain.

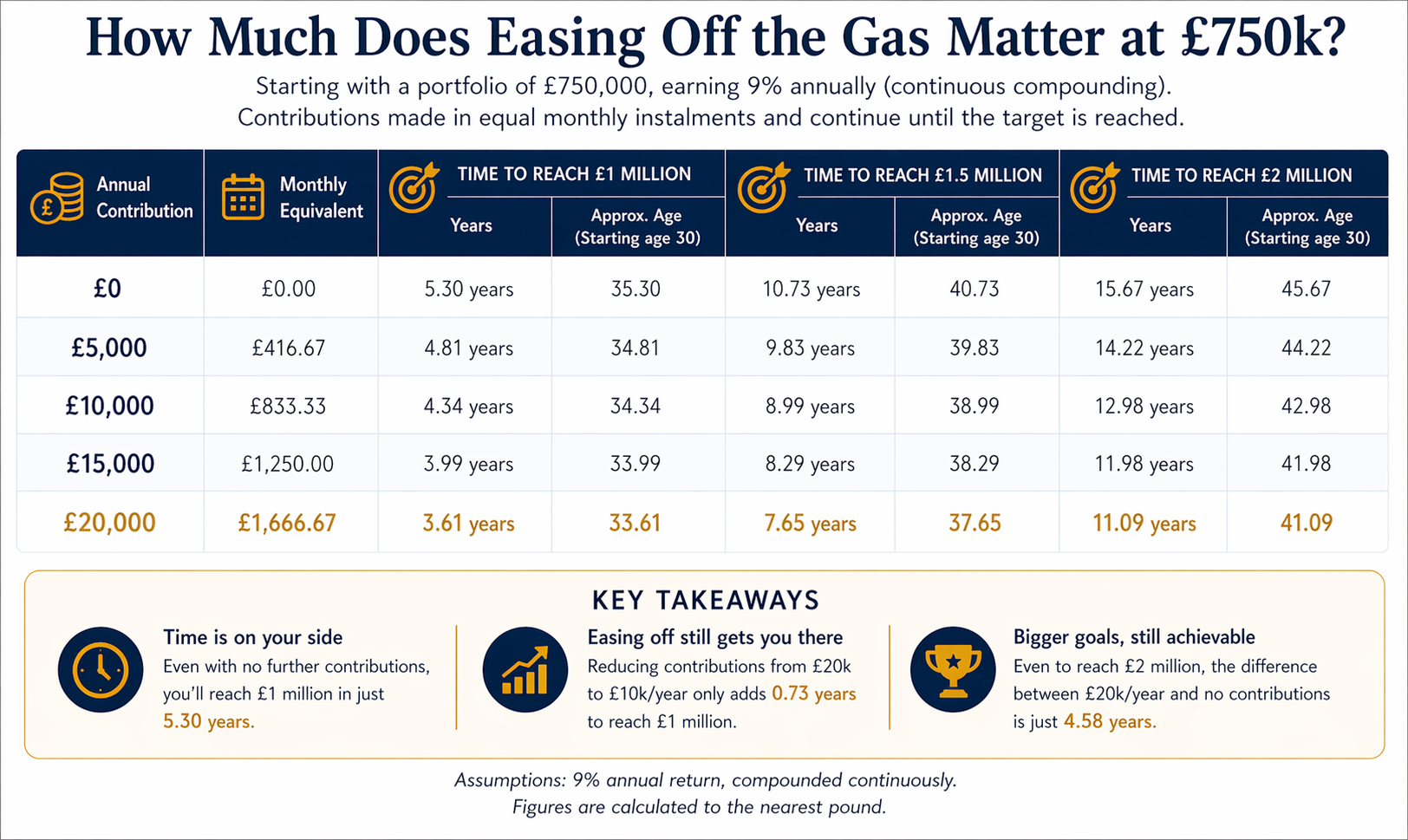

A £750,000 portfolio

Let’s take an idealised example: you’ve done very well and built a portfolio of £750k (by learning how to invest in the stock market, living a slower life, managing your personal finances like a business, and keeping your investing fees low).

This portfolio is globally diversified, earning around 9% annually over the long term. You’ve been contributing £20k diligently every year for years, but you now have options. You could:

- Keep contributing £20k per year.

- Reduce to £10k or £5k per year.

- Or even stop contributing altogether.

What impact does this actually have? Here’s what the numbers say:

Does easing off investment contributions really matter?

At higher portfolio values, easing off investing contributions has less impact than most people expect, because compounding becomes the primary driver of growth.

At this stage, compounding is doing most of the heavy lifting. Even with no further contributions, the numbers are striking:

- £1 million in ~5.3 years.

- £1.5 million in ~10.7 years.

- £2 million in ~15.7 years.

Now compare that to continuing contributions:

- £20k/year gets you to £1 million in ~3.6 years.

- And to £2 million in ~11.1 years.

Yes, contributing more still helps, but the difference is smaller than many people expect.

You have flexibility at high portfolio values

This is the real takeaway.

Once your portfolio reaches higher levels – £500k, £750k, and beyond – the pressure really eases. You’re no longer relying solely on your income to build wealth. Your investments are now contributing meaningfully on your behalf. Whether you continue to contribute or not makes little difference in the long term. Your portfolio will still continue to grow and you will become enormously wealthy.

You can still make substantial progress towards your long term goals while:

- Reducing your savings rate.

- Changing careers.

- Working fewer hours.

- Taking a dream holiday every year.

- Or simply enjoying more of your money along the way.

These things won’t make much difference in the decades ahead.

Final thoughts

In the early stages, discipline matters most. Saving, pound-cost averaging your investments, and staying consistent are what matter most when building wealth up to £500k. But beyond that, the game changes.

It’s no longer about maximising every contribution. It’s about balancing portfolio progress with how you spend your time and your quality of life. You can now afford to take your foot off the gas to spend your money and time more meaningfully – compounding now keeps your investment vehicle on cruise control.

If you enjoyed this article, you might also find the following helpful:

- Don’t Dance with the Stock Market

- The 4% Rule – how to know when to retire

- How to make the most of your ISA

You can follow me on X, and find me on Pinterest, Instagram and Facebook.

Leave a Reply