So, you’ve just started your career, and as a young 21 year-old, are looking at the insurmountable amount of money you’ll need to pay for all the expensive things in life you want, like a car and a wedding. Not to mention a house – and that long-distant dream: retirement.

It can feel overwhelming. On an average salary, is it even possible to build real wealth – or are you destined to work your entire life just to get by?

In this article, I’ll show you how to build wealth in the UK on a median salary using a simple, consistent strategy – and how, with time and discipline, you can build a portfolio worth millions.

How to build wealth in the UK (quick answer)

The simplest way to build wealth in the UK is to consistently invest through a workplace pension and a Stocks & Shares ISA, using low-cost index funds. Over time, compounding does the heavy lifting – even on an average salary.

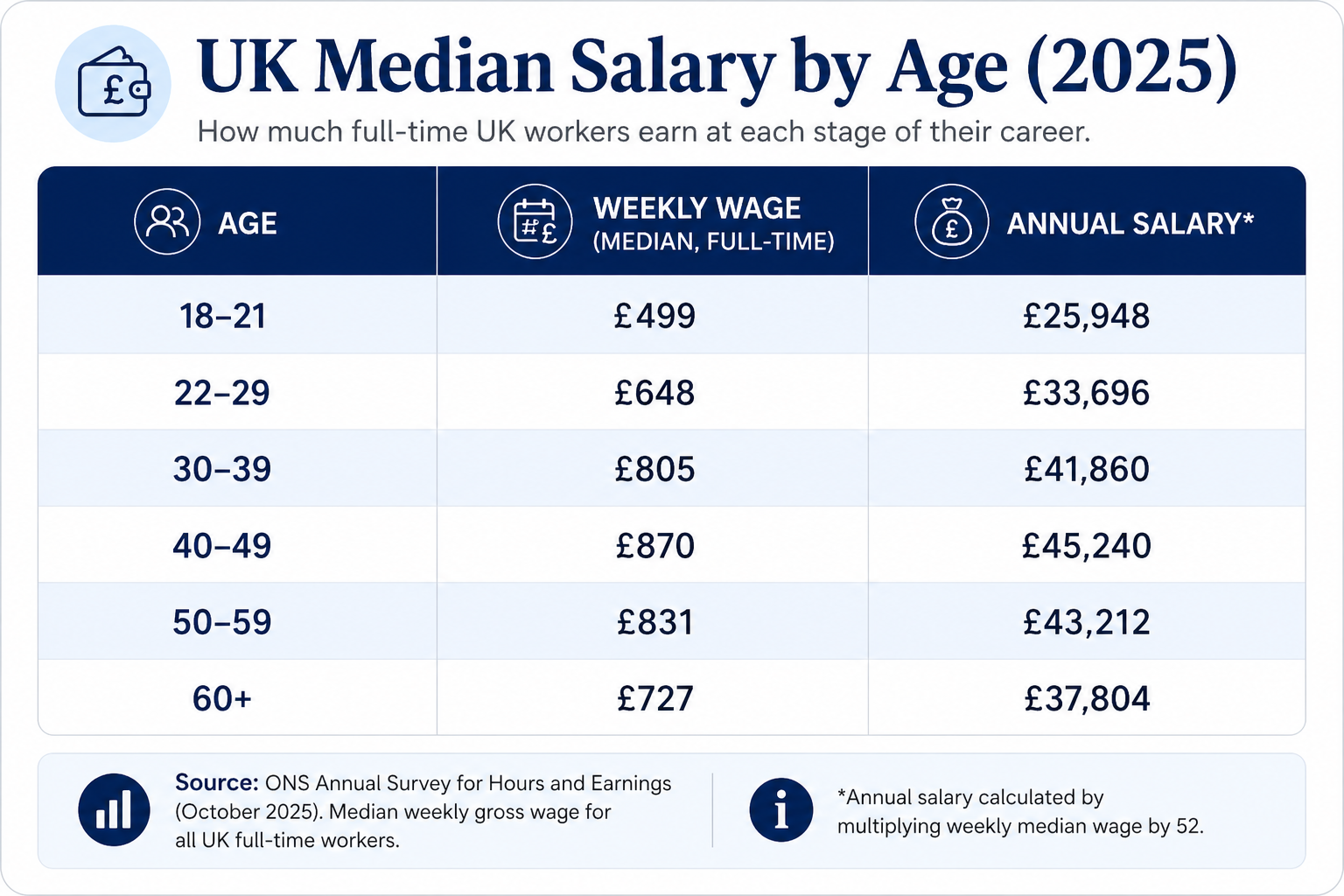

UK median salary

Your name is Joe Average, and you have the foresight to be well-versed in financial education, and came across this website early in life. You’ve read all the books I recommend, and have already opened an account with Vanguard. It’s all with good intentions, but you still have no money to your name. So you get a job at Deskjob Corp. The initial salary is £26,000, and you earn a median wage through the rest of your career.

Here’s how that would look:

How pensions build wealth over time

Your employer offers the standard workplace pension (5% employee contribution + 3% employer contribution), which you take advantage of (they’re giving you free money, after all). You move this into an index fund tracking the global stock market with rock-bottom costs, like Vanguard’s FTSE All-World UCITS ETF.

In Year 1, that means an annual contribution of £2,405. In subsequent years, the contributions grow as your annual pay increases. Here’s how that looks:

The pension pot grows to almost £1.2 million in value, after working and contributing for 39 years (up to age 60). That’s a staggering amount of money, and proves unequivocally that investing early and consistently into low cost index funds is a significant wealth builder in the long-term.

Using a Lifetime ISA for additional growth

You also start investing into a Lifetime ISA. Unfortunately, Vanguard doesn’t currently offer Lifetime ISAs. However, the opportunity to take an immediate 25% government bonus every year (on a maximum £4,000 contribution) is too good to pass up. So you open a Lifetime ISA with JPMorgan Investing (formerly Nutmeg), accepting that they have relatively high fees:

You can open a Lifetime ISA at age 18, and put in up to £4,000 each year until you’re 50. You can withdraw money from your ISA if you are:

- Buying your first home.

- Aged 60 or over.

- Terminally ill, with less than 12 months to live.

The growth on a £5,000 investment each year (£4k from you, plus £1k government bonus) will look like this:

So, assuming that you max out your LISA and pension contributions every year, you could have a total of (£1.68 + £1.19) £2.87 million upon retirement at age 60.

But what about inflation?

Inflation is an important consideration as it slowly erodes the value of your money over time. Inflation in the UK has averaged around 4.1% annually since 1979, while real (inflation-adjusted) wage growth has been ~0.4% per year. This means that employees are slowly becoming richer and wage growth will (slowly) outpace inflation.

Yes, there will be (significant) inflation over your lifetime, but during that time, average wages will likely rise even more, and so pension contributions will increase. (LISA contributions would not increase – at least not according to current laws).

What about fees?

I have not detracted investment fees from my calculations. They are idealised scenarios. Returns in real-world investing would be lower, especially for the LISA with JPMorgan investing (which has fees close to 1% per year). Vanguard fees are low (0.19% per year for the FTSE All-World UCITS ETF).

Either way, it’s a lot of money from doing a few simple (but far from easy) things:

- Consistent pension contributions.

- Consistent LISA contributions.

- Staying the course and leaving your money invested throughout.

- Working for 39 years until age 60.

Percentage savings rate

The total savings rate is quite low, averaging 14.5% throughout your career, but around 17.7% before age 50 (when LISA contributions stop).

Based on these calculations, it’s clear that you do not have to have a high savings rate to build a very large retirement portfolio. But you are committed to a 39-year working career. Fortunately, it does not have to be this way for Joe Average:

What happens if you stop saving?

Here’s how LISA contributions could stack up:

Even stopping saving at age 35 leads to a huge retirement pot. You contribute £180k less than someone who keeps working until age 60, but end up with around 70% of the final wealth.

Most of the heavy lifting is done by the early contributions, not the later ones. The money you invest in your 20s and 30s matters far more than the money you invest later.

So, even on a median salary, Joe could theoretically stop saving from age 35, and enjoy spending 100% of his salary for the remaining years.

However, retiring at age 35 is a completely different story; Joe needs to find a way to fund the intermediate years before he can access those retirement savings.

Can you retire early on an average salary?

One way to do this would be to sacrifice the Lifetime ISA completely, and instead just invest into a normal ISA. Savings in a regular ISA can be accessed tax-free at any time. Joe needs to build enough of a buffer in his ISA to last him until he can access his pension at age 55 (or age 57 from April 2028). How can he do this?

Well, it is possible – but very aggressive. It would be dangerous to assume the age at which you can access a private pension will stay at 57 forever. As people live for longer into retirement and claim their state pension for longer, the government has to find ways to reduce their expenses (and the national debt of £2.8 trillion(!)). It’s plausible the pension age will increase again in the future. So, you’d want a buffer to reach your pension withdrawal age with.

In the below scenario, we leave in an ~£95,000 buffer at age 60, and assume an initial withdrawal of £25,000 per year from age 35, adjusted annually upward for inflation by 4% each year (this is slightly more aggressive than the 3% annual adjustment for inflation assumed in 4% rule calculations, but in-line with UK annual inflation since 1979). Such a withdrawal strategy would get you safely to personal pension withdrawal age:

To do this, you’d need to save an average of £1,142 per month from age 21-35, on a median salary. That is… pretty aggressive. In fact, for much of that time, it would require a savings rate of more than 50%:

However, given the principles we discuss regularly on Slow Down and Save, achieving such a high savings rate isn’t out of the question; it might require some inventive solutions such as living with Mum and Dad for the first few years, and not driving (or having a very cheap car). But with some dedication it’s certainly achievable.

The goalposts are always moving

In the simulations I’ve done here, we assumed a steady rate of inflation and return from the stock market. Of course, neither is steady (far from it in fact). Inflation ebbs and flows with the national and international geopolitical climate, while the stock market is, by its nature, volatile. Savings rates during your working career and then spending in retirement are rarely steady either. Life gets in the way – sometimes to your advantage (like a promotion), and sometime not (like a stock market crash).

The key is to be flexible, and be able to react to the moving goalposts. You can always work for another few years to ensure you have:

- Greater savings.

- More in your workplace pension.

- Fewer years on which to draw down from your pension.

Even in retirement, you can go back to work if you want. (And in fact, it’s more common than you think.) Retirement is never final. Alternatively, you can vary your savings rate while working as your life permits, reduce spending during retirement to shore up your savings, or start a side-hustle or business that generates income. Perhaps the best way to fast track your route to financial success is to be a fantastic employee and get a pay rise (or multiple pay rises).

Whatever you decide to do, there are plenty of options available. By being more intentional with how you save and spend money, it’s certainly possible for someone on a median salary to retire a multi-millionaire, and to even retire in their mid-thirties if they really put their mind to it. The research in this article proves that it is possible – it’s now down to you to make it happen!

I wish you all the best in that journey.

Yes – building wealth on an average UK salary is entirely possible with consistency and time. By regularly contributing to a workplace pension and a Stocks & Shares ISA, and investing in low-cost index funds, you allow compounding to do most of the work. You don’t need a high income – you need discipline, patience, and a long-term mindset.

There’s no single number, but consistency matters more than the exact amount. In the examples I’ve produced for this article, a combined savings rate of around 10-20% over a full career is enough to build substantial wealth. Higher savings rates can accelerate the process, but even modest contributions, invested consistently over decades, can grow into a significant retirement portfolio.

Absolutely, but it requires a high savings rate. In the example I show, retiring at 35 is possible with aggressive saving – often 40-60% of income in the early years.

When you start matters more. Contributions made in your 20s and 30s have far more time to compound, meaning they contribute disproportionately to your final portfolio value. Starting early reduces the pressure to save large amounts later, while delaying investing means you have to work much harder to achieve the same outcome.

Invest regularly through a workplace pension and a Stocks & Shares ISA, using low-cost global index funds. Automating your contributions, increasing them gradually over time, and staying invested through market ups and downs is often enough. You don’t need complex strategies – just a simple plan and the discipline to stick with it.

Thank you for reading this article. Here are some others you may enjoy:

- How to Make the Most of Your Workplace Pension

- How to make the most of your ISA

- The Major Money Milestones as you Build Wealth

- Retire Early by Not Being a Moron with Your Money

- How a Millionaire Is Made £3.50 at a Time (The Small Money Mindset That Builds Wealth)

You can follow me on X, and find me on Pinterest, Instagram and Facebook.

Leave a Reply